|

||||||

|

|

|||||

|

||||||

Category Archives: ~ politics petitions pollution and pop culture

JUSTICE: Uncertainty Around DADT

Last week, the Justice Department asked Judge Virginia Phillips to stay her broad injunction barring the military from enforcing the Don’t Ask, Don’t Tell policy until it has an opportunity to appeal the decision to the U.S. Ninth Circuit Court of Appeals. In the appeal notice that accompanied the stay request, the government argued that ending enforcement of the policy “before the appeal in this case has run its course will place gay and lesbian servicemembers in a position of grave uncertainty.” “If the Court’s decision were later reversed, the military would be faced with the question of whether to discharge any servicemembers who have revealed their sexual orientation in reliance on this Court’s decision and injunction,” the government wrote. “Such an injunction therefore should not be entered before appellate review has been completed.” Meanwhile, the Department of Defense has also issued new orders via email late Thursday afternoon “informing all five branches of the military that they must comply with an injunction ordered by a federal judge” until the judge grants the government’s request. The Pentagon warned gay and lesbian servicemembers against changing their behavior in the interim. “We note for servicemembers that altering their personal conduct in this legally uncertain environment may have adverse consequences for themselves or others should the court’s decision be reversed,” Under Secretary of Defense for personnel and readiness Clifford Stanley wrote on Thursday.

FRUSTRATION OVER APPEAL: DOJ‘s appeal of the decision comes after intense lobbying from House and Senate Democrats — including House Speaker Nancy Pelosi (D-CA) — to allow the recent ruling to stand. As DADT scholar Nathaniel Frank explained, “The court case, I think, is one of the more likely now, for the President to say, this actually is unconstitutional and although there is a tradition of defending standing law, it’s not obligated to defend a policy that it believes is unconstitutional.” President Obama has previously implied that DADT is constitutional and Republicans and two Democrats successfully filibustered repeal in the Senate (the measure passed the House in May). But Obama has consistently argued that he would continue to try to repeal DADT through the legislative process to accommodate the work of the Pentagon’s ongoing review. “I don’t think it’s too much to ask, to say ‘Let’s do this in an orderly way’ — to ensure, by the way, that gays and lesbians who are serving honorably in our armed forces aren’t subject to harassment and bullying and a whole bunch of other stuff once we implement the policy,” Obama told Rolling Stone magazine in late September. The appeal comes a day after Secretary of Defense Robert Gates warned that ending the ban is “an action that needs to be taken by the Congress and that it is an action that requires careful preparation, and a lot of training.” “It has enormous consequences for our troops,” Gates said, ignoring research by the Center for American Progress’ Larry Korb, Sean Duggan, and Laura Conley which has found that repeal is actually a simple process and has been completed without incident by many other countries, including some of our closest allies.

MILITARY RESISTANT TO CHANGE: Gates, along with other military leaders, has resisted and delayed changing the policy before the Pentagon releases its review of the ban during the first week of December. Following Gates’ remarks, The Palm Center established a website to track his prediction that the court’s decision to suspend the policy would have “enormous consequences,” including all reported instances of harm to unit cohesion, discipline and privacy that have arisen during this period of open gay service. “Now that the ban has been suspended, we are searching vigilantly for such consequences, and we will use the new web site as a hub for reporting what we find,” Palm Center Director Aaron Belkin said. Last week, the group also submitted a Freedom of Information Act request for all documentation of reported negative consequences of the suspension of DADT. Meanwhile, the Pentagon task force that has been studying the consequences of ending the policy, is “well along” in formulating its recommendations, and officials don’t expect ruling or the moratorium to affect its work. According to some military officials, “[t]he task force found deep resistance to the idea of repealing the law in some elements of the armed services, especially within the combat units, an officer familiar with the findings said. But the surveys also have found segments of the military who were not overly worried about allowing gays and lesbians to serve.”

ENDING THE BAN THROUGH CONGRESS: During an MTV/BET/CMT sponsored town hall on Thursday, Obama told young voters that the policy should be repealed by Congress, not through an executive order or the courts. Distinguishing himself from President Harry Truman — who desegregated the armed forces via executive order in 1948 — Obama explained that “the difference between my position right now and Harry Truman’s was that Congress explicitly passed a law that took away the power of the executive branch to end this policy unilaterally. So this is not a situation in which with a stroke of a pen I can simply end a policy.” Obama stressed that he’s been able to convince Gates and Joint Chiefs of Staff Chairman Mike Mullen to support repeal and promised that the policy would end “on my watch.” “But I do have an obligation to make sure that I’m following some of the rules,” Obama said. “I can’t simply ignore laws that are out there, I’ve got to work to make sure that they are changed.” On Thursday, White House Press Secretary Robert Gibbs promised that Obama would work to end the policy during the lame duck session of Congress, telling the Advocate’s Kerry Eleveld that the President would be “actively involved in that.” Obama should also suspend discharges using his stop loss authority, thus ending the discharges of qualified men and women during wartime.

Share this:

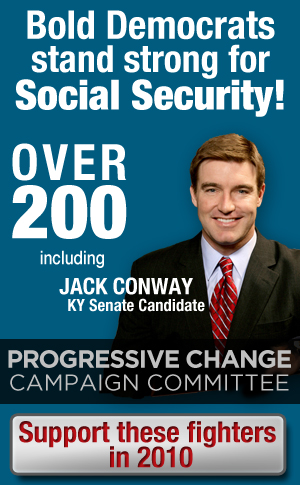

A major announcement

Rand Paul, the Tea Party leader running against me for Senate in Kentucky, thinks Social Security is unconstitutional. Other Republicans across the nation are also campaigning on privatization and Social Security cuts.

With a Tea Party deep on the fringe, the way for Democrats to win in 2010 is to have a spine — and go on offense.

That’s why today, I am proud to announce with my friends at the Progressive Change Campaign Committee that over 200 congressional candidates and members of Congress are promising to oppose any cuts to Social Security.

We’re saying no privatization, no raising the retirement age, no messing with the best program for seniors and workers in American history — and no mincing words about it.

We’ll make sure the political insiders and the media take notice of where the grassroots want Democratic leaders to be.

The PCCC has done a great job working with me and other Democratic candidates to go on offense on Social Security — and I’ve been taking the Social Security fight directly to Rand Paul in debates, speeches, and media events.

The 200 others include:

- Senate candidates Scott McAdams (AK), Roxanne Conlin (IA), Lee Fisher (OH), Alexi Giannoulias (IL), Kendrick Meek (FL), Paul Hodes (NH), Elaine Marshall (NC), and others

- House candidates Ann McLane Kuster (NH), Joe Garcia (FL), Bill Hedrick (CA), Rob Miller (SC), Julia Lassa (WI), Manan Trivedi (PA), Ed Potosnak (NJ), Michael Oliverio (WV), and others

- Members of Congress Raul Grijalva (AZ), Mary Jo Kilroy (OH), Alan Grayson (FL), Michael Acuri (NY), Carol Shea-Porter (NH), Ed Potosnak (NJ), Bill Owens (NY), John Boccieri (OH), and others

- The full list is at SocialSecurityProtectors.com

As Rachel Maddow would say, “This is what it looks like when Democrats go on offense.”

Then, please pass this email to your friends who want bold Democrats. Thanks for being a bold progressive.

Jack Conway

Share this:

RE: Russ Feingold

|

Russ Feingold’s opponent is Ron Johnson, a millionaire who’s spent $5.2 million of his own money trying to buy Russ’s Senate seat.

Ron Johnson supports NAFTA. He likes the Patriot Act. He thinks speaking out against the war is “extremely harmful to our nation.”

Lucky for us, Russ got Johnson to agree to three debates. Now Ron Johnson going to have to stand next to Russ and defend his extreme positions to Wisconsin voters.

FDL activists stepped up for Russ big time two weeks ago, raising more than $38,000 for his campaign. We want to show Russ and Wisconsin voters that ordinary people want to see Senator Feingold return to the Senate next year, not a self-funded millionaire.

http://action.firedoglake.com/feingold

Russ stood alone and opposed the Patriot Act. He opposed FISA. He opposed the wars in Iraq and Afghanistan. And he’s done the same thing no matter who controls Congress or the White House. He always put principles before party.

Russ is locked in a tough battle, but he’s fighting hard. He’s got 22 field offices across Wisconsin, more than any campaign in country, and his supporters are working hard to turn out voters.

But a lot is riding on these debates. We want Russ to know going into them that we’ve got his back, so we set a goal of $50,000. We’re almost there – can you please chip in to make sure Russ Feingold can continue to fight for what’s right?

With your help, we’ll show Wisconsin voters that principle counts over party; that people power will prevail over a self-funded millionaire who wants to buy his way to the Senate.

Thanks for supporting Russ, and for all you do.

Jane Hamsher

FDL Action PAC

Share this:

Temper tantrum -repost-

Last month, Republican Senate candidate Joe Miller said that Republicans must have the “courage to shut down the government.” Republican Congressman Steve King recently demanded a “blood oath” from House Minority Leader John Boehner to ensure the full repeal of health care reform — even if it means shutting the government down.

And former House Speaker Newt Gingrich, mastermind of the disastrous government shutdowns of the 1990s, has been crowing about a potential shutdown for months.

For Republicans, what once seemed radical is now wholly in the mainstream.

Even worse, they are pulling in huge donations from special interests who are comfortable with a shutdown that hurts the American people — so long as it gets them what they want.

We won’t stand by and watch this happen — and that’s why we’re growing the By the People Fund.

Grassroots Democrats have given 2.9 million donations to show that our voices won’t be drowned out by special-interest donations to fuel a special-interests agenda. Now we need to keep up the pace to reach our goal of 3 million individual donations — we need 20,000 contributors this week to hit the mark.

Can you donate $5 to help us keep growing the By the People Fund today?

All around the country this fall, Republicans are trying to convince voters to hire them for a job. But they keep saying that one of the first items on their agenda would be to go on strike.

A government shutdown would cut off the programs, benefits, and services relied upon by millions of seniors, veterans, and families around the country. Veterans’ hospitals would be closed; Social Security checks would not go out.

This is the political equivalent of a temper tantrum — and it hurts those who need help the most.

With just more than 40 days until the election, it’s time for us to step up.

We’ve got organizers on the ground in all 50 states, and we’re doubling down on efforts to register new voters and turn out the supporters who’ve helped us win all across the country.

The meaningful changes we’ve fought for and won have always been built on the energy and support of people like you.

So if you’ve been wondering when might be the best time to pitch in where you’re able, the time is now. And if you’re sick and tired of the notion that simply because Republicans are yelling louder, we are willing to go quietly — then it’s time for you to raise your voice.

I know that we can win this fall — but it’s going to take all of us.

Please donate $5 or more to the By the People Fund today:

http://my.democrats.org/Shutdown

Thanks,

Governor Tim Kaine

Chairman

You must be logged in to post a comment.